Hitting PAR; Neutral $52 PT (No Paywall)

Why PAR is a long-term winner in the enterprise restaurant technology industry but near-term headwinds will act as an overhang for shares to appreciate

For all readers, I recommend opening the file below this paragraph. The file is titled "PaxDex Research—Hitting PAR; Neutral $52 PT." I have created a much better-formatted equity research report for this write-up. But the entire research report is also located here for anyone who likes to read long-form text on this platform. As always, Feel free to ask any questions!

PaxDex Research—Hitting PAR; Neutral $52 PT

Initiation Introduction

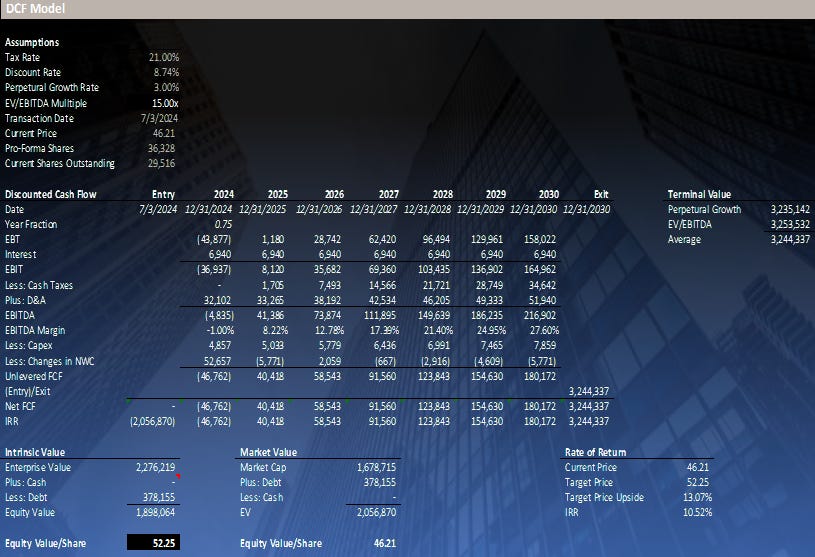

I am initiating coverage on PAR Technology (PAR: NYSE) with a neutral rating and a $52 price target or 5.5x 2025 ARR on my estimates. I want to continue to cover PAR and its developments to possibly make it a position as it's a small-cap that will inflect into profitability over the next 18 – 24 months while trading at a discount to its comparables. The Company has recently sold off its non-core cash cow asset, proving that its fast-growing core business is ready to carry the business profits, and management has made two strategic acquisitions this year that will prepare the company to win several enterprise RFPs. However, near-term headwinds like onboarding costs for major customers, acquisition integration, and a crowded shareholder base where the buy-side is expecting profits to inflect in H2 2024, which I believe will be pushed out close to H2 2025/H1 2026 will result in PAR unable to inflect into share price appreciation. To sum it up in a couple of sentences, I believe PAR is poised to emerge as one of the few winners in the global enterprise restaurant point-of-sale (POS) and software market that is sticky and counter-cyclical. However, near-term delays in profitability will remain an overhang for shares to appreciate.

Cloud Point-of-Sale Importance

Before talking about PAR specifically and the company overview, I think it would be helpful for readers to understand how vital a POS system is to a restaurant at any level, from a mom & pop pizza restaurant to an enterprise with thousands of locations like Burger King. To first understand the point-of-sale importance you want to know what the POS system is actually doing for a restaurant, it isn’t just something that you insert, swipe, or tap your credit card on, and you get charged. When you insert, swipe, or tap your credit card, that POS system charges your card, recognizing your order in the system to then re-display it on the chef’s screen in the kitchen to cook the food and then ultimately transfers the money back to the restaurant and this is just 10% of what a POS system does for a restaurant. To elaborate more on the importance of a POS… Before PAR, Toast, Agilysis, Oracle, or Square (These companies are other POS providers), restaurants would use on-premises systems (like NCR Aloha). The big breakthrough in the restaurant POS industry was taking the software to the cloud which opened up API’s and new services for restaurants that can be layered onto the traditional POS. Things like online ordering, inventory management, drive-thru ordering, payroll management, extend financing, let you book reservations, and POS systems have integrated other third-party companies like DoorDash, UberEats, etc… To when an order gets placed on that 3P app like DoorDash it pipes that order directly into the POS to make sure the order gets re-displayed back into the kitchen, so the food is ready when the carrier picks up the food for delivery. A POS system acts as the central nervous system of the restaurant's operations

Company Overview

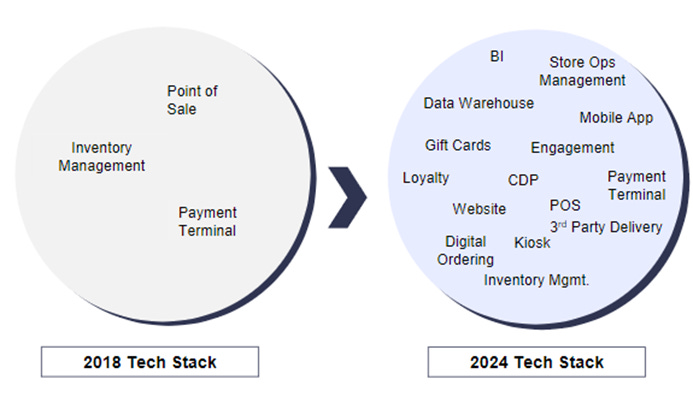

PAR Technology Corporation, is a restaurant technology company that provides unified commerce solutions for enterprise restaurants. Simply put, PAR operates and provides POS and software that primarily targets restaurants with 25+ locations. Below is PAR’s history of how it has become a leading restaurant technology company in the enterprise space through several key acquisitions.

Brink POS—acquired in September 2014 for $15mm. Brink is the anchor cloud POS system; it acts as the brain of the restaurant, connecting everything into one location. Brink POS also enables PAR Payments, a product that enables various payment options (online, in-store, mobile app, 3P) for a restaurant.

DataCentral – acquired in November 2019 for $42mm; originally named “Restaurant Magic” and rebranded to Data Central, it provides back-office solutions (inventory, accounting, analytics, payroll management).

Punchh – acquired in April 2021 for $507.7mm Punchh is a customer loyalty and engagement software designing reward apps for companies and engagement campaigns.

MENU – acquired in August 2022 for $18.4mm, offering branded online ordering solutions to restaurants. MENU is partnered with DoorDash, Grubhub and Uber Eats and this product has low switching cost, meaning it’s a feature, not a product (bear case for ticker OLO).

Stuzo – acquired in March 2024 for $190mm, providing customer engagement programs like reward apps and other loyalty programs specifically to gas stations and other convenience stores (C-stores).

TASK – acquired in March 2024 for $206M, allows restaurants to build custom-tailored customer engagement programs, like reward apps. It also sells AURES POS and ordering kiosks to restaurants. TASK is PAR’s way of expanding internationally, as TASK generates 78% of its revenue outside of the U.S.

Long-Term Industry Trends

I want to take this section of the initiation to talk about the restaurant tech industry and the four dynamics I believe will play out over time. The first is addressing a risk that could play out: the risk that enterprises, because of their scale, can create their own POS and tech stack in-house, cutting out any need to choose a vendor like PAR. I find this outcome very unlikely when considering even a massive chain like Restaurant Brands International (RBI), the holding company of Burger King, Tim Hortons, Firehouse Subs, and Popeyes totaling over 30,000 restaurant locations. RBI has ~1,200 corporate employees, say 15% of that is IT, so ~180 employees, and the company announced late last year that they had chosen PAR Brink POS and MENU for all its U.S. Burger King locations. So, even if one of the largest enterprise QSR chains couldn’t build out its own tech stack, what would make a chain with 1,000 locations even close to being able to do it? Clearly unlikely.

The second idea starts with the fact that restaurants want one provider for POS, as it simplifies operations, employee training, customer loyalty programs, and the restaurant’s back office. Additionally, if a restaurant has multiple POS vendors, less data will come in, and competing algorithms will result in worse customer results. Furthermore, cloud POS systems are very sticky once installed in a restaurant. Unless the POS system has significant downtime or cannot have additional tech layered, it’s doubtful a restaurant will replace it. Below is a quote from a restaurant chain with over 100 locations.

“POS system switch out in a restaurant is one of the most painful and difficult things to do” - COO of Beef o Brady

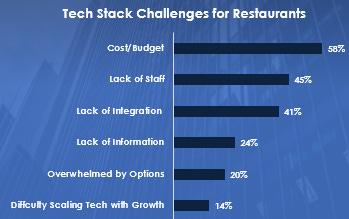

Brands are suffering from restaurant tech complexity because the industry is still in its early years of growth and trying to find product-market fits with dozens of cloud POS providers to choose from. Not every player is equal, and that will play out over time.

PAR has had 100% uptime and leads in the tech space, with over 200+ APIs layered onto Brink POS. The company's acquisitions clearly identify PAR's full suite of restaurant solutions. PAR can act as the one-stop shop for an enterprise restaurant tech stack, allowing each acquisition to have significant long-term cross-selling opportunities.

Another topic I want to discuss is how AI will impact the restaurant tech industry. One of the early things that I believe will be adopted is AI voice drive-thru ordering. This is pretty simple to understand but extremely complex in reality. Eventually, restaurants won’t need to allocate physical labor to drive-thru orders, saving the restaurant cost and creating a customer for a restaurant tech company that provides the AI voice ordering technology. Additionally, since the restaurant tech industry is still so early, we have yet to see most large enterprises have a sole vendor for restaurant tech; as the industry matures and enterprises single into one vendor, it will allow restaurant tech companies like PAR to accumulate a significant amount of data as there won’t be competing algorithms anymore and it will enable predictive analytics. What does predictive analytics mean? I think restaurant tech will get to a point where, let’s say, for example, a restaurant with omnichannel ordering, it’s a Friday night where the restaurant is getting so many orders to the point it can’t fulfill them all, the POS systems algorithm will automatically predict this spike in orders and stop accepting orders from DoorDash or Uber Eats as they have the lowest margin for the restaurant.

To summarize, the dynamics in the enterprise restaurant technology industry I believe will play out long-term:

1) The risk of enterprise customers creating their tech stack in-house is improbable

2) Enterprise customers will choose one sole vendor for their most important tech stack (POS, back-office, loyalty)

3) Players that solely operate a “feature” like OLO will either go bankrupt or be acquired for pennies on their 2020-2021 valuations

4) AI voice ordering and predictive analytics will enable higher APRU in the future

TASK & Stuzo Strategic Acquisitions

On March 11, 2024, PAR announced its acquisition of TASK and Stuzo. TASK is an Australian-based food service transaction platform offering international interactive customer engagement tools (loyalty programs/reward apps) tailored for enterprises and restaurants worldwide. TASK manages the loyalty/app program for major brands like McDonald's and Starbucks Australia. Additionally, TASK has a cloud POS system, AURES, which is sold to SMBs/enterprise restaurants and other retailers. PAR acquired the company for $206mm in partly cash and stock, which put the company at 4x 2025 ARR for a company growing 30% YoY, running with double-digit operating profit margins, achieving the Rule of 40.

Stuzo, like TASK, is a digital engagement software provider that increases customer loyalty to drive more consumer wallet and customer lifetime value toward convenience and fuel retailers (C-Stores). Stuzo provides software for customer loyalty programs and apps to customers like Wawa, 7-Eleven, BP, and others. PAR funded the Stuzo acquisition via a $190mm private placement. Stuzo was acquired at 4.75x 2023 ARR (~$40mm ARR LTM) for a company with 40%+ EBITDA margin and a revenue CAGR of 56% from 2020. Again, the Stuzo acquisition achieves the Rule of 40 with ease.

As mentioned in the company overview, PAR has effectively acquired and built an entire restaurant tech stack, allowing them to win significant enterprise RFPs and market share. Moreover, I believe the opportunity to cross-sell existing products like Brink POS to C-Stores is likely.

Growth Drivers

1) Market Share (Wave of RFPs)

Several growth drivers fall within PAR taking market share, and some I already touched on, like restaurants wanting one vendor to cover their entire tech stack, which benefits PAR as it’s a one-stop shop for a restaurant's tech stack. However, what has also been seen is a lack of focus from Toast going down market into the enterprise (possibly starting to change, which I touch on page 12) space in recent years. It’s allowed PAR to, I believe, emerge as the #1 restaurant tech provider for enterprises. Last year, Toast lost its largest enterprise customer, Jamba Juice, and Punchh's competitor, Olo, lost Subway (15,000 locations) and continues to underperform as a stand-alone loyalty engagement service as it has turned out to be a feature, not a product.On

Below is a quote from management recently describing the incoming wave of RFPs

“We feel like we're in the beginning of that tidal wave. I'd say just in this quarter we've seen more RFPs and interest from the largest brands in the world than we have in my entire time at PAR as it relates to POS. And we also see that in loyalty within Punchh.” – Savneet (CEO), Q3 2023.

Restaurant Brands International (Ticker RBI) chose PAR Brink POS and MENU to be in all of their U.S. Burger King locations (~7,000); I believe this leads to RBI choosing PAR for its other brands, Popeyes, Tim Hortons, and Firehouse Subs. In the immediate future, assuming the Burger King rollout goes well, I believe RBI will choose PAR for its other 14,000 Burger King restaurants internationally. For context, Brink POS currently serves ~25,000 locations, if RBI chooses PAR for the rest of its brands and locations it would double Brink POS business from one customer. Furthermore, since the enterprise market has very long cycle, over time, I believe PAR will be able to up-sell products like Punchh or Data Central to existing enterprise customers.

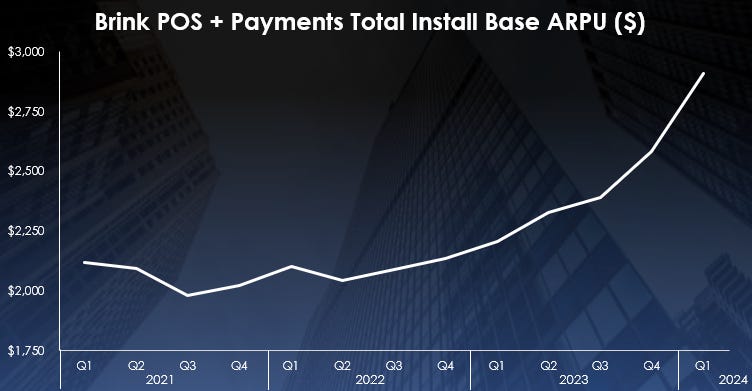

2) Price Increases

PAR has already started increasing prices on its premium product, Brink POS; below are the past quarters of incremental ARPU from customers who added Brink to their tech stack.

Note that in Q1 2024, the drop in ARPU is related to PAR changing how it accounts for its “Operator Solutions” segment. This segment has historically only included Brink POS and Payments, but as of the latest quarter, it now includes Data Central, which has an ARPU of ~$1,700. That’s why we saw incremental Brink ARPU go from $8,000 in Q4 2023 to ~$5,000 in Q1 2024. This chart shows that Brink is a premium product that accepts a price in return for customer ROI.

The average APRU for PAR’s total install base is up and to the right; I foresee this continuing

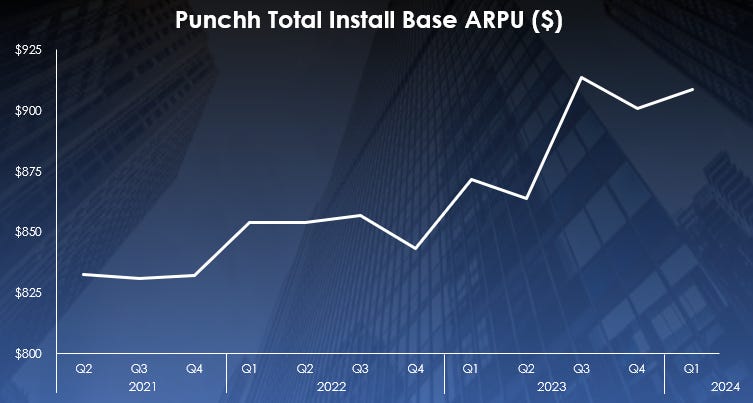

PAR’s second ARR segment, “Guest Engagement,” now includes Punchh, MENU, and now Stuzo. It will also include TASK once the acquisition is completed in Q3 2024. Punchh makes up the bulk of this segment, with ~60% attributed to Punchh, Stuzo making up ~40%, and MENU making up very little as PAR is just starting to monetize the $18.4mm MENU acquisition. Punchh has little to no pricing power on a standalone basis; therefore, pricing hasn’t moved much over the past few years, as shown below.

Where the ARPU will increase for the “Guest Engagement” segment is from Stuzo. Stuzo has a premium product compared to Punchh and dominates the C-Store end market, charging 2x—2.5x Punchh loyalty products. Assuming static pricing in this segment, the ARPU will naturally increase as Stuzo’s 40%+ growth rate is substantially higher than Punchh’s ~10%.

3) International Expansion

PAR’s recent acquisition of TASK opened up an entirely new and fast-growing international end market. Since PAR’s end customers are large enterprises/QSRs moving internationally, the strategy is not changed much or at all. This allows TASK’s point of sale system (AURES) to act as the beachhead to cross-sell Punchh, MENU, and Data Central to international customers. Currently, PAR’s U.S. customers want to expand and are growing faster internationally; what TASK enables for PAR and the considerable synergy here is PAR can go to its U.S. customers who are growing faster internationally and in need of best-in-class restaurant tech and say, “Hey, we know you are expanding internationally and are in need of tech, well, we just acquired an internationally player with an amazing cloud POS that we can layer Punchh, Data Central, MENU, and payments on top of.” International expansion is where the puck is going for North American restaurant tech players, and PAR is skating toward it.

4) C-Stores Expansion

With the acquisition of Stuzo, PAR now has the #1 (Stuzo) and #2 (Punchh) provider of customer loyalty software for C-Stores. Before the acquisition of Stuzo, PAR invested millions in SG&A and R&D to compete against Stuzo, but it lacked them sustainably. In fact, Stuzo, a customer loyalty product like Punchh, was taking more share and growing faster than Punchh while charging 2.0x – 2.5x per customer. But now that PAR has acquired Stuzo, it will allow revenue synergy from increasing prices and cost synergies as PAR won’t need to invest so much into Punchh’s R&D and SG&A to compete.

5) Core Business Focus

On June 10, 2024, PAR announced that it had sold its low margin cash producing government services segment to Booz Allen Hamilton (Ticker BAH) for $102mm. While this doesn’t drive the future growth of the underlying business, it indicates management focus and profitability prospects. PAR’s recent divestiture of its government services segment, which was its asset that serviced the balance sheet, likely proves that the restaurant retail brand will be ready to stand on its own two legs and become profitable. Furthermore, it simplifies PAR’s story to now be solely a restaurant tech company. As well of note, the mix shift of eliminating low government services margins will drive COGS down, I estimate, ~14.0% post divesture.

Headwinds Resulting in Share Price Stagnation

1) Toast Breaking Big into The Enterprise Market

“Now, inside the four walls of a restaurant, the needs of enterprise restaurant chain are no different than they are for SMB.” – Toast Investor Day 5/29/24

Toast has built a firm grasp on the independent restaurant market and has started to move down the market to add locations. This implies that Toast is seeking to add more enterprise customers today than it has in the past; additionally, I’d think Toast will expand internationally, which could have a similar ARPU to the U.S. independents, but that ARPU is still to be determined. Moving down-market into enterprises directly competes with PAR. Toast has been investing significantly in tailoring its tech stack to enterprises, thinking of AI drive-thru voice and other AI-leveraged capabilities. This is where I think Toast could have a better tech stack overall than PAR. Toast is 7x larger of a company than PAR, which allows it to invest significantly more into product/software development than PAR, which doesn’t mean Toast will become the #1 enterprise player, but it’s a risk worth watching and seeing how enterprise RFPs play out. An interesting thing of note, however, as I mentioned earlier Toast's largest enterprise customer, Jamba Juice, kicked it out in replacement of Qu late last year. Unsure as to why Toast was replaced, but as today stands, PAR has a dominant market share over Toast as PAR serves Dairy Queen, Subway, Burger King, Sweet Green, Five Guys, Cava, etc. PAR’s Brink POS is mandated in all stores.

2) Continuous Customer Ramp Costs + Potentially Crowded Shareholder Base

As Burger King picked PAR to roll out its Brink POS and MENU products late last year across all 7,000 U.S. locations, it forced PAR to sustainably increase costs ahead of product rollout, which will start in Q2 2024. In fact, it diluted annual operating margins by ~2.00 – 2.50% from increased headcount and IT development. The costs should be quick to come down as the rollout occurs, but it signals future large enterprise deals, whether it’s an international rollout to Burger King (~14,000 stores) or adding new enterprises Tim Hortons + Popeyes (~9,200 stores), McDonald’s (~42,000 stores), etc. Each time, there’s a high chance that a significant amount of up-front costs will be needed and, in a moment, where hundreds of enterprise's RFPs will be bid on over the next few years, I can see a scenario where PAR’s consensus for profitability in H2 2024 continuously gets pushed out until RFPs slow down as ramp costs burden them.

Three hedge funds or private investors that make up almost 20.0% of PAR’s shareholder base: ADW Capital, Greenhaven Road Investment Management, and Voss Capital. All three are very pubic in their projections on PAR with each of them expecting profitability in H2 2024, if this does not come to light, I’d think there’s a >50% for a substantial selloff.

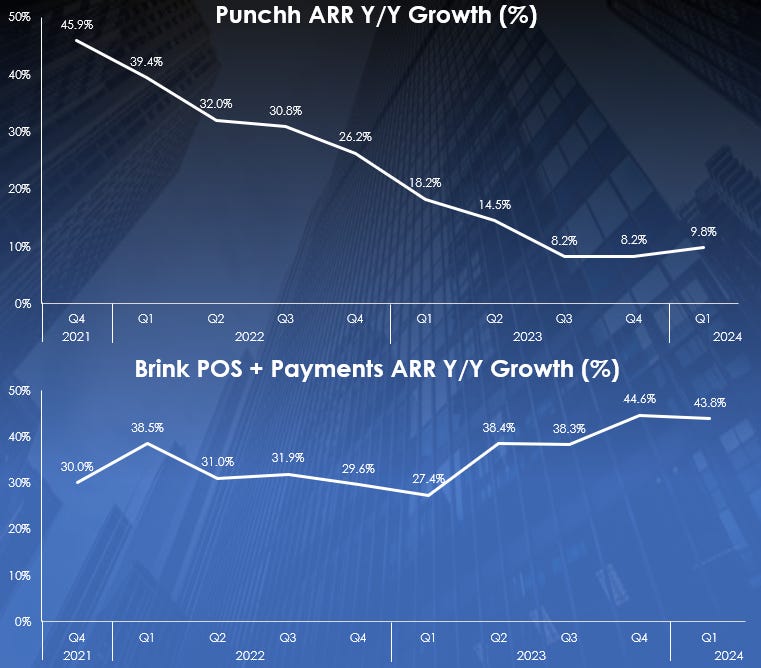

3) Punchh Needs to Accelerate

Since 2021, Punchh’s ARR Y/Y growth rate has been on a precipitous decline, falling from 40% to sub-10 %. It is also materially underperforming PAR’s other ARR segment, Operator Solutions, which is made up of Brink POS and payments. However, Punchh's trend of decelerating growth seems to be flattening, which could accelerate new wins from the coming wave of RFPs. The acquisition of Stuzo takes out one of its largest competitors.

4) Weak Balance Sheet

As PAR has spent more than $1.00bn on acquisitions, it funded some via cash, convertible debt, share issuance, a private placement, and selling of the Government business for $102mm. Given the core business won’t be able to generate enough cash to service the balance sheet until at least 2026/2027 I find it likely PAR will need to raise additional capital through either debt or share issuance, and most likely the ladder.

5) Valuation and Punchh Growth Concerns

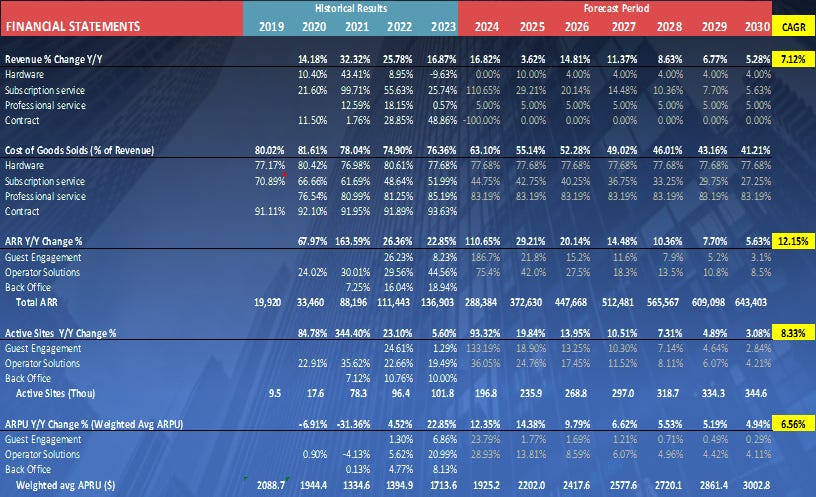

Put simply, at $46/share, PAR is priced for growth. In 2025, assuming ~19.8% active site growth, ARPU growth of ~14.4% (price increases inflecting), with Stuzo + TASK growing at their historical rates, PAR trades at 9.1x 2025 EV/GP. For a yet to be GAAP profitable company whose ARR growing at 29.0% YoY and whose total revenue is closer to ~21.3% (Ex Government Sale) is a demanding valuation to buy in at.

True Comps?

It's hard to find a true competitor for PAR. Sure, there are other cloud POS providers and restaurant tech companies, but none compete solely in the enterprise market. The closest competitor, in my mind, is Agilisys (AGYS). It, too, provides POS systems to enterprises but in the hotel chain industry, serving Marriott and Hilton. However, this implies that given the two operating in the enterprise space, they will have low churn rates due to high switching costs to a 1,000+ enterprise restaurant chain switching out POS systems. This is something that TOST must fight with as it serves primarily the independent SMB restaurant end market and has significantly more competition from Clover, Square, ShiftFOUR, and more. Furthermore, Toast revenue is derived mainly from a take rate on payment volume; take rates could quickly come down with fierce competition.

Combining it all, I believe PAR should most closely trade in line with AGYS, which trades at 13.6x forward EV/GP with ARR growing 20%+ for the next couple of years and EBITDA margins in the high teens. As it stands today PAR’s EBITDA margins next year will be MSD – HSD with ARR growth in the mid-twenty %. The discount between AGYS and PAR will close over time as PAR reaches profitability, so again, it’s the question of whether ramp costs hinder near-term profitability.

Model Assumptions

1) Volumes (active sites) to grow at a 6.7% CAGR through 2030 driven by enterprise RFP wins and international and C-Store expansion.

2) Price increases (ARPU) to grow at a 8.3% CAGR through 2030 driven by Brink POS price increase, payments mix shift, and Stuzo pricing power

3) EBITDA Margins going from (1.00%) in 2024 to 27.60% in 2030 driven by the government divesture, cost flattening, and incremental high-margin ARR

Income Statement Assumptions

DCF Assumptions

To sum it all up in a couple of sentences, I believe PAR is poised to emerge as one of the few winners in the sticky and countercyclical global enterprise restaurant point-of-sale (POS) and software market. However, near-term profitability delays will remain an overhang on shares' appreciation. I want to continue monitoring PAR’s developments to see if profitability can inflect sooner than I expect or if the valuation comes down. It’s a business I want to own long-term and hope to do at a discount to its intrinsic value.