ROKU 1Q25 Earnings Recap (No Paywall)

Gross profit numbers are going lower, upcoming tough comparisons, but an underlying Platform business that is continuing to grow at mid-teens y/y

Roku (ROKU) Earnings Recap & Notes:

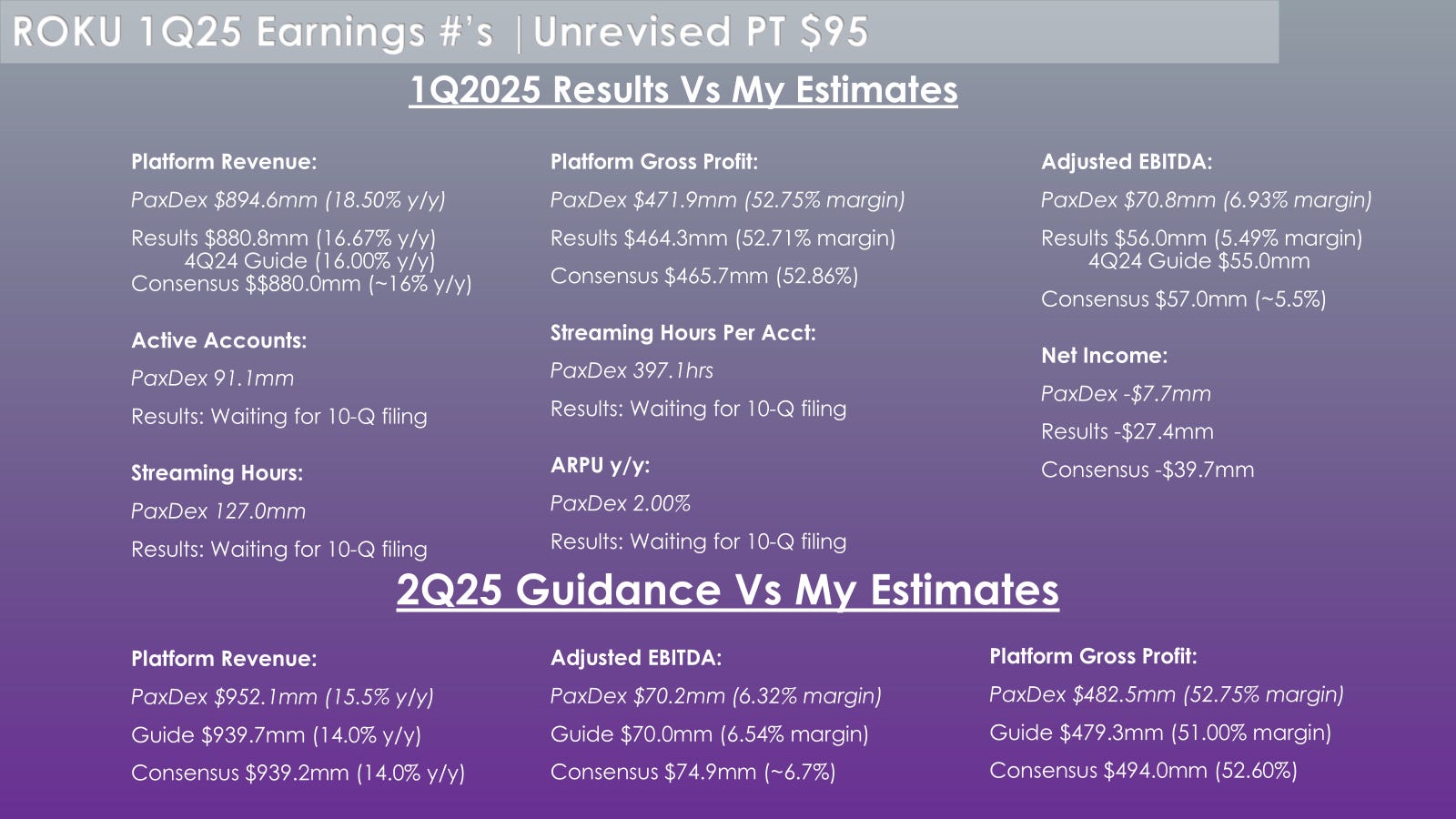

Yesterday, after the bell, ROKU reported its 1Q25 earnings, with mixed results. The Company lowered its FY25 Gross Profit guidance from $2,005mm (11.10% y/y) to $1,975mm (10.94% y/y) driven by a mix shift to a slightly lower Platform gross margin (~51%) vs. the initial guide in February for (~53%) due to advertisers switching from guaranteed ad campaign contracts to non-guaranteed ad campaign contracts (which come in at a lower gross margin). Due to macroeconomic uncertainties, advertisers are shortening their purchasing cycles to a week-to-week basis. The Company maintained its FY25 Platform revenue guidance of $3,950mm (11.20% y/y) and Adj. EBITDA target of $350mm (7.70% margin). Additionally, management adjusted its FY25 Net Income losses from $40mm to $30mm, driven by a $10mm step-up in other income.

Summary:

Near-term numbers will be revised lower due to gross margin headwinds related to shortening advertising buying cycles, which could drag on the stock if investors don't give ROKU credit for these headwinds being temporary. Additionally, upcoming tough comparisons (4Q25) will likely put near-term investors on the sidelines as fears surrounding the 4Q25 growth rate will linger. Furthermore, tough comparisons are exacerbated by ASC-606 adjustments from last year, which were $16mm in 2Q24, $12mm in 3Q24, and ~$5mm in 4Q24. However, if you back out the $16mm 606 headwind for 2Q25, Platform revenue would accelerate sequentially to ~17% y/y. Lastly, operating expenses and SBC came in slightly lower than expected, which I model will carry on throughout the year.

I increase my Platform FY26 growth rates from 11.9% y/y to 12.3% y/y (consensus 11.4% y/y) as I believe one-time headwinds such as 606 adjustments and tariff-related uncertainty (will both not exist in my view next year) are masking an underlying Platform business that is continuing to grow at mid-teens with comps easing following 4Q25. Additionally, the stock is down ~35% since February and now trades at ~12.2x FY26 EV/EBITDA (On $575mm FY26 EBITDA) for an asset with a several-year runway to grow EBITDA in the double digits, will reach 4-quarters of GAAP profits in FY26 opening up new index inclusion opportunities, and with signficant whitespace remaining in its core growth pillars. If there's weakness tomorrow, I am a buyer.

Key Points:

Consensus Revisions: Near-Term #'s Going Lower Due to Gross Margin Headwind

Management is guiding to a ~51% Platform gross margin in 2Q25, following its 1Q25 Platform gross margin of 52.71%, and a ~52% Platform gross margin for FY25. If you assume a 51.25% Platform gross margin from here on out through 4Q, Platform margins end up at 51.58% for the year (42bps lower than management FY guide), implying that the gross margin guide is back-half weighted. That said, I think the back half weighting is correct due to the past month being the trough in tariff-related fears, and advertisers will gradually gain more certainty from this point onward through year-end, resulting in a more favorable mix shift for Platform margins back to their ~52% - 53% initial guidance range back in February.

Consensus FY25 Platform gross margins are 53.14%, which will need to be revised to ~150bps lower (~$50mm in GP dollars). This would be the primary reason the stock trades lower tomorrow, if it does.

Comp's Headwind: ASC-606 Adjustments & 4Q Politcal

In 2Q24, there was $16mm in revenue recognition adjustments (ASC-606), 3Q24 $12mm, and 4Q24 ~$5mm. These will drag on revenue growth throughout the rest of FY25, with the upcoming quarter experiencing ~200bps y/y revenue growth headwind related to 606 adjustments. However, backing this adjustment out, revenue growth would increase sequentially (based on management 2Q25 guide) with Platform up ~17% y/y. As time progresses into FY26, tailwinds related to lapping these quarters should provide a ~50 - 200bps revenue growth y/y tailwind.

4Q25 will be a very tough comparison as last year in 4Q24 political drove signficant growth, but more importantly, it held back many non-political ad dollars until December 2024, which inflated 4Q numbers. When asked about the cadence of growth in FY25, the CFO came off as hesitant about believing in teen Platform growth in 4Q25, which would be a material deceleration in the growth rate and likely sideline some investors or make ROKU a popular short based on decelerating growth rates (even if unrelated to the underlying businesses trajectory).

Bright Spot: Opex Growing Slower Than Expected

SBC and operating expenses came in a tad lower than expected, and I believe this will continue as management optimizes expenses while turning on the monetization in oUSA regions like LATAM. I assume OpEx, as a percentage of revenue, will decline by 301bps in FY25 and 315bps in FY26.

My price target increases from $95 to $97 per share. Reach out if you'd like to see my assumptions and/or model behind the price target.

Earnings Call Notes:

What gives you confidence in reaffirming your full-year revenue and EBITDA guidance?

ROKU-specific positives are overcoming macro uncertainty

Shift to streaming secular trend, advertisers have already begun shifting from linear to streaming

Macro uncertainty makes advertisers look for higher ROI, which ROKU’s platform can provide

Business model, since the last advertising downturn (2022), has significantly diversified through less reliance on media & entertainment end market, deeper integration with DSPs, ROKU platform still has a lot of ad supply to sell, billing 10s of millions of subscriptions more since 2022

Reaffirming platform revenue and EBITDA assumes a slight weakening in macro

Advertising market update?

Seeing shifts in advertisers' budgets that the cycles are shifting more toward short-term frames, contracts are on a week-to-week basis, and are non-guaranteed commitments

Programmatic advertising (on the ROKU platform) is what advertisers want in this environment, so they can adjust their spend if needed. This benefits ROKU vs traditional linear TV ads

Idiosyncratic drivers are currently offsetting the macro. Can this continue if the macro deteriorates further?

Seeing a shift from guaranteed to non-guaranteed ads, which drives more volume toward ROKU

Initiatives in growing subscriptions and supply of ads sold can continue to offset macro

Advertisers are asking for more measurement of ad performance, which benefits ROKU due to their platform being newer/with lots of investment in helping advertisers understand the benefit of ROKU’s platform advertising

What is the best way to think about programmatic to platform revenue growth? Is it just a mix shift/cannibalization thing? Or more incremental?

The multi-year push by ROKU to diversify demand is working, and this shift of programmatic growth is incremental

Think of programmatic as an avenue to purchase ads, not a whole other product. This is driving more incremental growth, and SMB use Roku Ads Manager, which is all net new to the ROKU platform.

Investment in tools/measurements is helping ROKU take more market share in a macro downturn/uncertain ad market

How does The Roku Channel becoming #2 on the platform change the conversation with content providers?

The Roku Channel (TRC) engagement grew 84% y/y, and there’s a large amount of inventory to sell

Roku is the leader into television streaming

TRC does not cost a lot to get the content, but it outputs a significant amount of engagement to build the strength of ROKU's assets

Why don’t you think the virtual MVPD market is a transitory market going to zero?

Linear channels are still very popular and growing on the ROKU platform (consumers like to flip through old content)

Why doesn’t the Frndly TV acquisition aid your bundle of ad services, and why doesn’t it look backwards into the linear TV space?

Frndly is a linear TV brand that is a paid tier of linear channels that are very popular

Brand on Frndly that can be elevated because it's being moved onto ROKU’s platform

Frndly acquisition adjusted EBITDA margin is accretive vs ROKU

Can you explain the logic behind not packaging and not selling the first part of your data for CTV?

Roku has a 100% authentic audience, and 50% of broadband U.S. households are viewing from the Roku operating system

The best way to take care of partners is to take care of all their data, so in the short-medium term, the best opportunity is to create a differentiated ad platform and use their data with Roku’s

Ways to monetize Roku’s data have been discussed, but not in action yet

Is Frndly TV assumed in full year and 2Q guidance?

Frndly acquisition was assumed in the initial full-year guide back in 4Q24

With tariffs, what are you factoring into your guidance? Can you adjust tariff costs quickly, or does it take a while?

Manufacturing is through multiple partners in multiple regions

Based on the current tariff structure, ROKU does not expect a material change to Devices' gross profit guidance

ROKU has raised prices in response to some of the higher costs related to tariffs

ROKU players have a high market share in low-end TVs, which could mean that, in a weaker macro environment, consumers shift down from high-end TVs or extend their existing TV lives, which will benefit ROKU marginally

Can you walk us through how to think about platform revenue growth for the rest of the year?

Q4 will have a smaller growth rate in 4Q due to the tough comp (political environment)

Slight sequential step down in growth rate during 4Q

Lots of ASC-606 adjustments in 2Q24 with $16M and less so in 3Q and lesser extent in 4Q. ROKU has zero 606 adjustments this year, which is making comps quite hard

If you back out ASC 606 adjustments in 2Q24, the 2Q25 guide growth rate is actually the same 17%

Any advertising verticals that ROKU sees more traction in outside of media & entertainment?

Recently, Roku added a new row to the home screen with recommendations of content that helped drive The Roku Channel to grow 84% y/y

If we think about 2H24 and back out ASC 606 and political one-time headwinds, does the teens platform growth rate continue?

Over the longer term, absolutely can sustain teens' growth rate

Only hiccup will be 4Q with a decel, because there was so much volume after the political in the month of December

The 51% platform margins are a slight decline from recent quarters. What drove that?

In 1Q and 2Q, Roku has seen a shift from guaranteed to non-guaranteed, but that mix shift comes in at a slightly lower margin

If we go to a pre-macro concern, then margins will revert to 52% - 53% in 2H. In the current status quo, margins will continue to come in slightly lower than 52%

Over time, management thinks gross margin can grow, driven by higher volumes sold

In 4Q, management started by saying devices would grow 12%, and now management is guiding to flat, why?

Roku is not focused on Device revenues, but is focused on growth in Roku being used in households

Device revenue is through first-party sales, while third-party sales show zero effect in the Device segment

Device sales can be very lumpy quarter to quarter and management pays less attention to it. Units in terms of market share is continuing to grow in all regions.